Reverse Mortgages 101, from Santa Barbara Independent, Active Aging Special Section, July 30, 2020.

MUTUAL OF OMAHA’S MONTECITO OFFICE OFFERS PLANNING ADVICE

A type of loan available to homeowners aged 62 and older, reverse mortgages allow people to borrow money based on the value of their homes. Unlike other loans, the debt isn’t immediately due. Instead, payment is deferred until the borrower either dies or sells the home, at which point the debt comes out of their estate or sale.

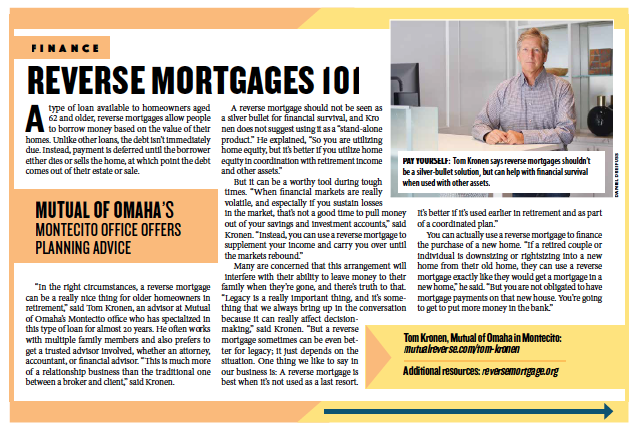

“In the right circumstances, a reverse mortgage can be a really nice thing for older homeowners in retirement,” said Tom Kronen, an advisor at Mutual of Omaha’s Montecito office who has specialized in this type of loan for almost 20 years. He often works with multiple family members and also prefers to get a trusted advisor involved, whether an attorney, accountant, or financial advisor.

“This is much more of a relationship business than the traditional one between a broker and client,” said Kronen. A reverse mortgage should not be seen as a silver bullet for financial survival, and Kronen does not suggest using it as a “stand-alone product.” He explained, “So you are utilizing home equity, but it’s better if you utilize home equity in coordination with retirement income and other assets.”

But it can be a worthy tool during tough times. “When financial markets are really volatile, and especially if you sustain losses in the market, that’s not a good time to pull money out of your savings and investment accounts,” said Kronen. “Instead, you can use a reverse mortgage to supplement your income and carry you over until the markets rebound.”

Many are concerned that this arrangement will interfere with their ability to leave money to their family when they’re gone, and there’s truth to that.

“Legacy is a really important thing, and it’s something that we always bring up in the conversation because it can really affect decision making,” said Kronen. “But a reverse mortgage sometimes can be even better for legacy; it just depends on the situation. One thing we like to say in our business is: A reverse mortgage is best when it’s not used as a last resort. It’s better if it’s used earlier in retirement and as part of a coordinated plan.”

You can actually use a reverse mortgage to finance the purchase of a new home. “If a retired couple or individual is downsizing or rightsizing into a new home from their old home, they can use a reverse mortgage exactly like they would get a mortgage in a new home,” he said. “But you are not obligated to have mortgage payments on that new house. You’re going to get to put more money in the bank.”

Originally published in the Santa Barbara Independent on July 30, 2020. To view the Active Aging Guide to Senior Life, Seen Through a Pandemic Lens, click here.